First and foremost, we hope you and your family are healthy and safe. We hope that any impact on you has been minimal, and that you are able to use this as quality time and appreciate home life. It is during these most challenging of times that the true spirit of humanity shines through. We are immensely grateful to all the people hard at work to keep us healthy, safe, connected and fed.

Farmland LP is up and running and fully operational

We want to provide you with Farmland LP’s thoughts on the potential impact of COVID-19 on farmland as an investment, our people, and the business.

Overall know that Farmland LP is fully operational, and we proactively made adjustments to make sure our people are safe while maintaining operations and growing food.

Impact on Farmland as an investment

Our investors in farmland are ahead of the curve and understand the value of investing in real assets. Farmland has been a top performing asset class for about a century, through good times and in particularly in times like these when other asset classes experience extreme volatility, impact from economic cycles, or money printing (which is just beginning to ramp up again). As farmland is “Essential Infrastructure” tied to food production, we expect very little to no negative impact on the value of our investment due to COVID-19. Farmland is even more resilient than other real assets such as apartment buildings (living spaces for people), which may be impacted a bit if the economy enters a recession and rents are impacted. More at risk are office buildings assuming more people work from home regularly. But all these real assets are more resilient than the stock or bond markets.

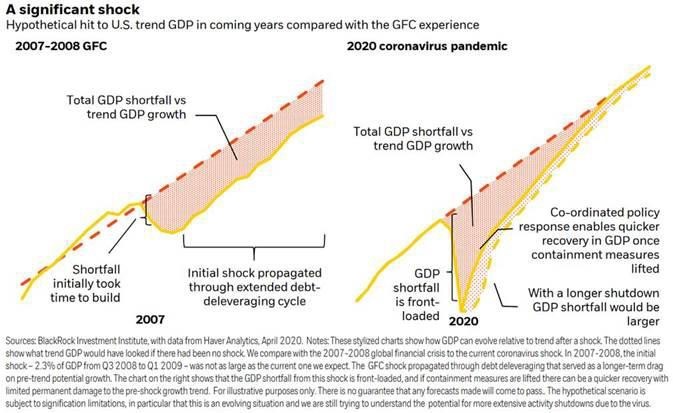

As investors, our eyes are on the trillions of dollars that will be used to fill the pothole in our $20 trillion annual GDP. The modern response is to print money sufficient to maintain normal leverage ratios and prevent a downward debt spiral, so in short, they will add approximately the amount of the lost GDP.

This chart compares 2008 to what they hope to accomplish now in 2020.

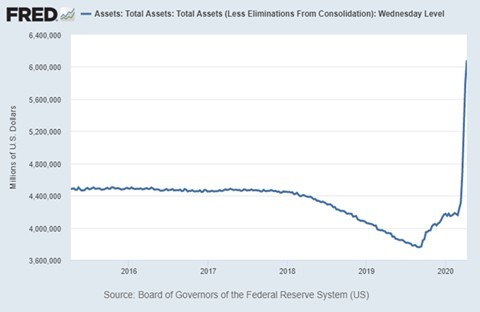

The Federal Reserve has already added about $2 trillion to its balance sheet. It took the Fed 4 years to add $2 trillion to its balance sheet from 2008 to 2013, and this time we did it in a month.

For context, there is only $2.7 trillion of Farmland in the U.S., and as a productive asset with limited supply, we expect the price of farmland to increase in dollar terms.

Our People are Healthy and Safe

I studied virology at UCSD, earning a degree in Biology while doing graduate research on HIV, the virus that causes AIDS (another type of pandemic). I also helped start a biotech company where we received FDA approval for a brain cancer therapeutic and we took the company public. So we built Farmland LP with the potential for pandemics in mind, along with climate change, economic downturns, energy/oil issues, and more (I like to think we are “pragmatic” rather than paranoid, but either way it pays off). And we were early to appreciate the potential magnitude of COVID-19, as this Coronavirus was on our radar January 27th.

We have two main business offices, one in San Francisco and one near Corvallis, Oregon, and much of what we do can be done remotely with Office 356, Dropbox, a virtual phone system (Teams), and hosted accounting software. We notified our SF team on March 8th to work remotely. Our Oregon office handles accounting, AP/AR, and HR, and initially we added a week of sick leave time and a zero tolerance policy for symptomatic employees to stay at home, however the following week we shut that office as well and they are now working remotely with one person collecting any non-electronic bills daily.

Our farm managers and farm workers are not crammed into crowded office buildings nor commuting on packed subways, so our farm team has relatively low risk exposure. That said, we enforce social distancing for our farm workers, and making sure our more senior and experienced (ok, older) farm managers are keeping their distance and leveraging the farm management web system we implemented over the past two years (Granular).

In summary, our 50 people are 100% healthy and we are working to ensure it stays that way. We see no material impact from this to our business nor to your investment in the farmland.

Impact on our Operations and Supply chain: Hope for the Best, Plan for the Worst

Each week on our farm management calls we kick off with a “Health and Corona” section, asking each manager for their thoughts on the following topics:

- Labor

- Supplies & materials

- Vendors

- Markets

- Long term impact

While we have made some adjustments, in general this is turning out to be business as usual for us. Here is the general status for each topic:

Labor. This is the area we expected the largest impact, however it appears that our employees are healthy and that labor contractors are looking for work. Our farm managers expect sufficient workers to be available, such as for organic blueberry harvest coming up in May.

Supplies and Materials. Just-in-time supply chains can be fragile, and our suppliers told us that we were the first firm to ask them if any of our materials originate in Asia, and thus may be potentially impacted by factory closures, transportation issues or personnel quarantines. Another benefit of using Certified Organic materials is that many/most are made locally (compost, etc.), and thus our supply chains are much shorter and local. That said, we pre-ordered and took early delivery of many materials to lock in current prices as well as to ensure our supply over the coming months.

Vendors. Most vendors seem fully operational. One vendor with some issues is our organic certifier Oregon Tilth which requires annual onsite inspections; however, their contractors are not visiting sites due to the virus. This would have potentially caused supply chain issues with supermarkets as the certificates would not have been current. That said, over the past week they appear to be modifying their policies and will likely work to certify us remotely.

Markets. Food distribution in the U.S. is divided into two main channels: About half of the food supply is distributed to consumers; and the other half to food service industries such as restaurants. That second channel to the food service sector is essentially shut down, and the farmers who served that channel have to make the switch to retail. These are the farmers you may have read articles about, dumping milk, lettuce, etc. Farmland LP is positioned well and is nicely diversified, with a good balance of markets. For example, we have a good portion of crops which end up in retail: frozen organic vegetables such as organic green beans and sweet corn; organic blueberries (fresh and frozen); and wine grapes. Overall, we expect the impact on income this year to be overall neutral to slightly down.

For insight, let’s divide the overall market into

The Good, The Bad, and The Ugly

The Good

- Fruit and vegetable demand is high as people are cooking at home

- Vegetables are up 41% the week ending March 15th vs 2019

- Fruits are up 27%

- Frozen vegetables are up more than 100%

- The USDA (via the Commodity Credit Corporation) two weeks ago purchased _all_ the holdover frozen blueberries in storage, which is expected to lift this crop’s price by 20c lb. This is the kind of support power the government has, and they are loading all cannons.

- Wine sales are up. My friend runs a large wine brokerage (BenchmarkWine.com) which had a record quarter. He said historically his average bottle selling price was $300, but last quarter the market bifurcated into two peaks. The first peak was at $50/bottle, due to increased immediate consumption, and the second peak was at $1000/bottle, for investment as people pulled cash out of the market and put it into collectible “liquid” real assets.

- So our green beans, sweet corn, blueberries and wine grapes are doing fine.

The Bad

- Milk prices are low and dropping, but that is not a new story. In our view dairy is not a good business to be in and we made a strategic decision to avoid investing in it many years ago. This should go in the ugly category but not because of the virus.

- Wheat prices dropped, but the futures market is 90% financial traders who never take delivery.

- The labor contractors are indicating they have enough labor, though we are watching this closely as we are planning our first blueberry fresh harvest. We have machines for harvest worst case, but we think labor will be available. Most other crops are machine harvested, as this is a key strategy for us.

- We do expect higher labor costs, both due to the need for securing extra labor due to a zero tolerance policy for people being sick and losing a % of the workers, plus additional costs for supplies such as gloves and masks.

- We have a small sale of non-irrigated land which is technically progressing, but the timing looks more uncertain. We’re not concerned about valuation though, and we have a backup buyer.

The Ugly

- Livestock producers who sell to restaurants and hospitality, which have all closed. Our lamb customer said his retailers are closed but he will still buy the lamb but may have to freeze it. Sheep are a 7-9-month crop, cattle are a 24-36-month crop, so the impact will vary based on that moving average.

- Commodity corn farmers, whose crop goes 40% to feedlots (restaurants aren’t buying) and 40% to ethanol (no one is driving).

- Similar situation for soy farmers

- For Farmland LP, demand for our seed crops which are bought by farmers are very slow.

- One tenant in Walla Walla, Washington grows potatoes, and the lack of French Fry sales is reducing contracted acres by 30% in Washington. We are expecting a switch in crops unless there is government crop/farmer support.

Long Term

We’re actively looking for problems, but we don’t see any long-term issues associated with the pandemic or the impact to the economy. Farmland is deemed “Essential Infrastructure” and food production is an essential service. If anything, we expect stronger demand for higher value organic crops.

We do hope for the best, but we actively plan for the worst, and from my viewpoint we seem well positioned for the current situation. For our investors, your assets are safe and appreciating, the employees are healthy and hard at work, and the business prospects are strong.

We sincerely appreciate your support and partnership and look forward to a rewarding future. Brighter days are ahead. For now, and always, please stay safe, healthy, and happy.

Sincerely,

Craig Wichner and all the Farmland LP team